Fixed Income: Friend or Foe?

Fixed income has been a friend to investors. Over the past 20 years, the annualised return to the end of last year for both domestic and global fixed income has exceeded global share returns. But with rates so low and bond prices so expensive, will fixed income become your foe?

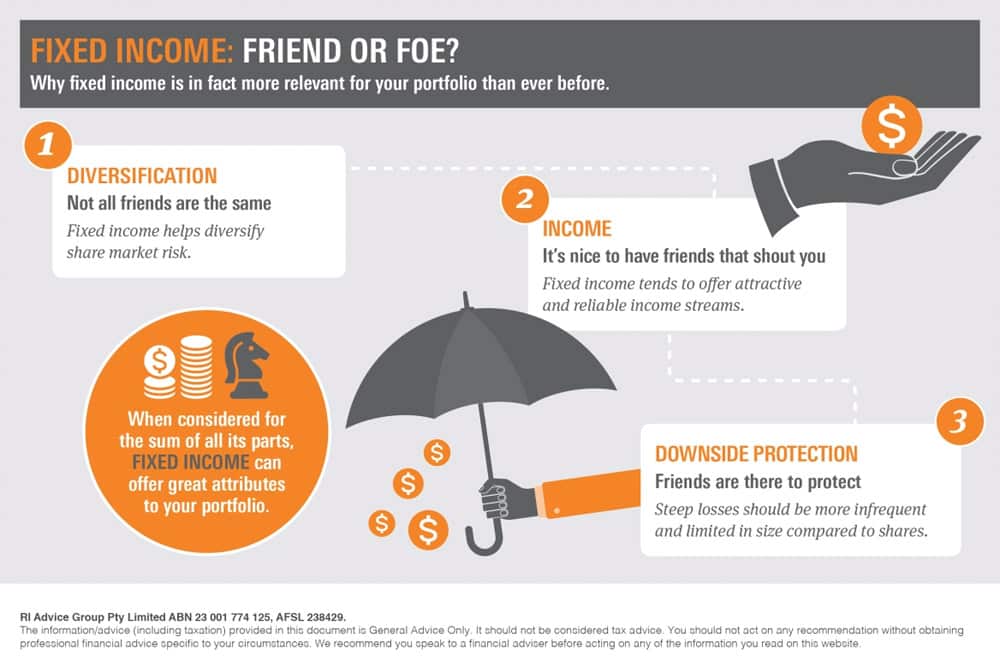

Read on to find out why fixed income is, in fact, more relevant for your portfolio than ever before.

Diversification – Not All Friends Are The Same

Traditional fixed income strategies play an important role in diversifying share market risk and cushioning portfolio returns during times of economic downturn. This is because fixed income returns generally have a low to negative relationship to shares. A negative relationship, or what is commonly referred to as a negative correlation, occurs when the value of one asset rises while the value of another falls. For example, in 2008 and 2011 Australian and global shares incurred large negative returns while fixed income funds posted strong positive returns.

Table 1: Australian and Global Equity returns verse Australian and Global Fixed Income returns in 2008 and 2011

| Year | Australian Shares | Global Shares | Australian Fixed Income | Global Fixed Income |

| 2008 | -37.7% | -28.4% | 11.2% | 3.6% |

| 2011 | -11.1% | -7.9% | 10.1% | 7.9% |

Source: Morningstar

Morningstar Categories: Australian Shares – Australia Equity Large Blend, Global Equities – World Equity Large Blend, Australian Fixed Income – Australia Fund Bonds – Australia, Global Fixed Income – Australia Fund Bonds – Global

The correlation between fixed income and shares can change over time and vary between different fixed income securities. Certain fixed income securities with higher credit risk, which is the risk that the issuer of the security will default, have historically become more correlated to shares when the share market is in freefall, while government bonds, with low credit risk, have generally remained a true diversifier.

Common Australian and global fixed income indices have a large proportion of their holdings weighted to government bonds. For example, the Bloomberg Barclay’s Global Aggregate index comprises of around 51% global government bonds. As traditional fixed income managers track these indices they will tend to hold a reasonable proportion of their portfolio in government bonds, and therefore continue to offer true diversification benefits.

Income – It’s Nice To Have Friends That Shout You

In addition to being a good diversifier, fixed income provides a positive, regular source of income returns. Income is provided by the coupon payments, which are essentially interest payments.

Currently, there are no investment-grade bonds (BBB or higher credit rating) that have been issued with a negative-rate coupon. So even if price returns for fixed income are negative, the income return via the coupon is currently positive. Even in Japan, where zero interest rate policies are in place, the coupon rate on investment-grade fixed income has remained positive.

Fixed income sceptics may point out that coupons are currently at very low levels. However, this is not to say opportunities don’t exist. Divergent interest rate cycles present opportunities for unconstrained bond funds.

Unconstrained bond funds are those managed without traditional indices or benchmark constraints. These strategies have the flexibility to ‘go anywhere’ and will invest across fixed income sectors, geographies and currencies. In practice this means unconstrained bond funds are able to tactically invest in countries where interest rates are rising and in emerging markets which offer higher yields. While this means taking on additional risk, there is the opportunity for higher returns.

Downside Protection – Friends Are There To Protect

Fixed income is designed to help provide downside protection, meaning that steep losses should be more infrequent and limited in size compared to shares.

Historically, this has been the case and is illustrated by the below graph. The graph shows the global bond index, Bloomberg Barclays Global Aggregate index in dark blue, where the largest drawdown over 25 years was 4.9%[1] in 1994. This negative return is relatively small compared to Australian and global shares which have had maximum drawdowns of -47.2%[2] and -48.3%[3] respectively.

Graph 1: Drawdown of global fixed income verse global and Australian shares

Source: Lonsec Global Fixed Income – Bloomberg Barclays Global Agg TR (AUD hedged); Australian Shares – S&P/ASX 200 TR Index AUD: Global Equiteis – MSCI World NR Index AUD

While negative returns for fixed income securities have been historically less severe when compared to shares, it is important to realise that just as friendships can have downturns, fixed income can also produce negative returns in certain periods of the investment and interest rate cycle.

For example, traditional fixed income strategies may struggle in a fast rising interest rate environment.

Nevertheless, certain unconstrained bond funds have absolute return targets and aim to achieve positive returns in all market conditions, including in rising interest rate environments. These style funds do not manage to an index and as a result typically have lower sensitivity to changes in interest rates.

Don’t Break It Off Just Yet

Those advocating a break-up are likely to tout that increasing interest rates are going to hurt fixed income funds, particularly the traditional variety. While in the short term there may be some pain, over the longer run a rising rate environment offers investors the opportunity to reinvest at higher interest rates (coupons), which is a positive.

Despite the US Federal Reserve hiking rates four times since December 2015, we have seen both Australian and Global Fixed Income return positive 2.5% and 2.7% over the last 12 months[4]

So when considered for the sum of all its parts, fixed income can offer great attributes to your portfolio. Whether it is traditional or unconstrained – each has different benefits to offer your portfolio making fixed income a true and long-term friend.

Contact Newcastle Financial Planning Group to learn more.

Disclaimer: The information provided in this document, including any tax information, is general information only and does not constitute personal advice. It has been prepared without taking into account any of your individual objectives, financial situation or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. From time to time we may send you informative updates and details of the range RI Advice Group Pty Ltd ABN 23 001 774 125 AFSL 238429

[1] BBgBarc Global Aggregate TR Hedged AUD Data from Morningstar between 1 Jan 1994 to 31 Dec 2016

[2] S&P/ASX 200 TR AUD from Morningstar between 1 Jan 1994 to 31 May 2017

[3] MSCI World NR AUD from Morningstar between 1 Jan 1994 to 31 May 2017

[4] Australian fixed income – Bloomberg Composite Bond All Maturities, International Fixed Income – Barclays Global Aggregate Bond Index (hedged) as at 31 May 2017